Senior Care vs Aetna Medicare Advantage PPO

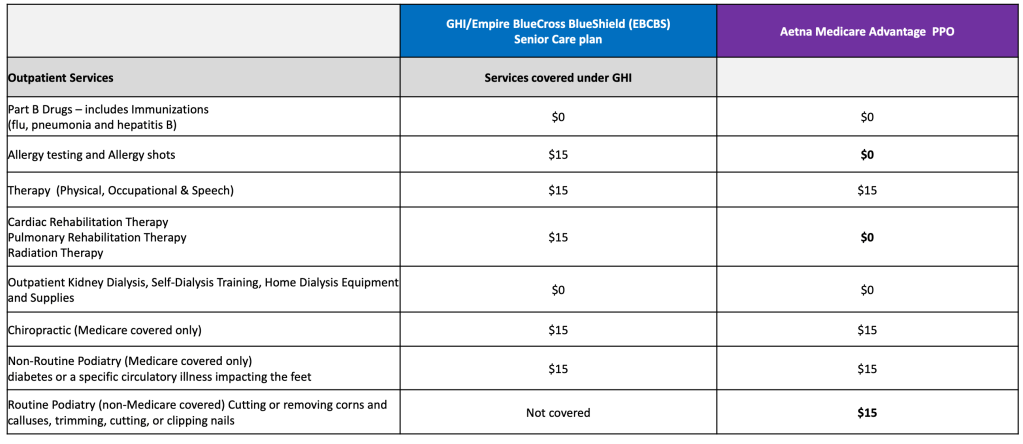

The UFT published a chart comparing GHI Senior Care with Aetna Medicare Advantage. In 15 categories the plans provide the same benefit at the same cost. In 25 categories Aetna is better. In no categories is Senior Care better.

I think Unity knows it is more complicated. I think they know that MA is the worse choice for some members, maybe most members. Let’s dig in.

Aetna Medicare Advantage PPO is the health insurance that most of our Medicare eligible retirees will be transferred to in September. That is, it’s the plan they will be transferred to if the current Office of Labor Relations/Municipal Labor Committee/UFT plan goes through,

Aetna 25, Senior Care 0, with 15 ties

And reading the chart, it’s a no brainer. Aetna 25, Senior Care 0, with 15 ties.

The actual situation is more complicated.

It’s more complicated

The chart does not include any information about how widely Aetna is accepted. The current claim is with 94% or 95% of the doctors who take Senior Care, with some provision for the others, but people are nervous about provisions to take care of something that before Aetna did not need to be taken care of.

The chart does not talk about changing plans. But once in a Medicare Advantage plan for a certain period of time (is it 6 months?) it either becomes difficult or impossible (I don’t know the precise mechanisms) to move back to a traditional Medigap.

The chart does not include information on prior authorizations. A separate email compares prior authorizations under the Aetna Medicare Advantage PPO with prior authorizations under the previous OLR/MLC/UFT Medicare Advantage plan (the “Alliance”). Aetna’s prior authorizations are more limited than the Alliance’s would have been. But there is no comparison of prior authorizations under Aetna vs prior authorizations under Senior Care. There really is no comparison – Aetna will introduce many prior authorizations that UFT retirees do not currently have. And people are right to suspect that more prior authorizations means more denials of care.

At the City Council hearings on the Administrative Code, five people, two former UFT officers (Unity) and three other Unity members, testified that they did not want to move to a MA plan (they were not arguing against MA in general, just for themselves.) Obviously even those in favor of this plan know about its limitations. But our union leadership is choosing to leave that out of the current – I don’t know – discussion? – debate?

Chart vs Trust

Look, all of this should require careful discussion. But it is really hard to talk to the people responsible for publishing that chart. The chart is deceptive, by omission. The chart undermines trust. The chart is part of a sales pitch, not a discussion. That chart is not part of a respectful exchange of views.

ps – I notice that the author of the chart (meaning the organization that produced it) is not indicated. But is on the UFT website. And it is linked in emails under Mulgrew and Murphy’s names.

The fact that they are comparing GHI & not traditional Medicare to the Aetna Medicare advantage plans is in my book a deceptive practice.

Will option be available to retain our current coverage? Will there be a premium? Cost?

Their current plan involves no option to retain Senior Care – that plan would end (I think).

You can go out and purchase your own medigap, but then you are out of the City plan, and lose all your reimbursements.

Also, Mulgrew said at the RTC (or maybe Sorkin said it?) that if you leave the City plan, your dependents do, as well.

Exactly!!

“Cost share waived for 2023”. WHAT DOES IT GO UP TO IN 2024?

The whole co-pay column for the comparison is an outright LIE! We don’t have co-pays now (thanks to the law suit) and you will have to pay $1500 out of pocket prior to their claim of no co-pays.

No Preauth on senior care plans , that should itself be a turn off on the MA plans